The Great Oil Pivot: Strategic Realignment or a Quiet Surrender of Leverage?

Let’s be honest.

For three years, India didn’t just buy oil. It bought breathing space.

When Russia was cornered in 2022 and Urals crude started trading at discounts of $15 to $30 per barrel, India stepped in without drama. No ideological positioning. Just procurement discipline.

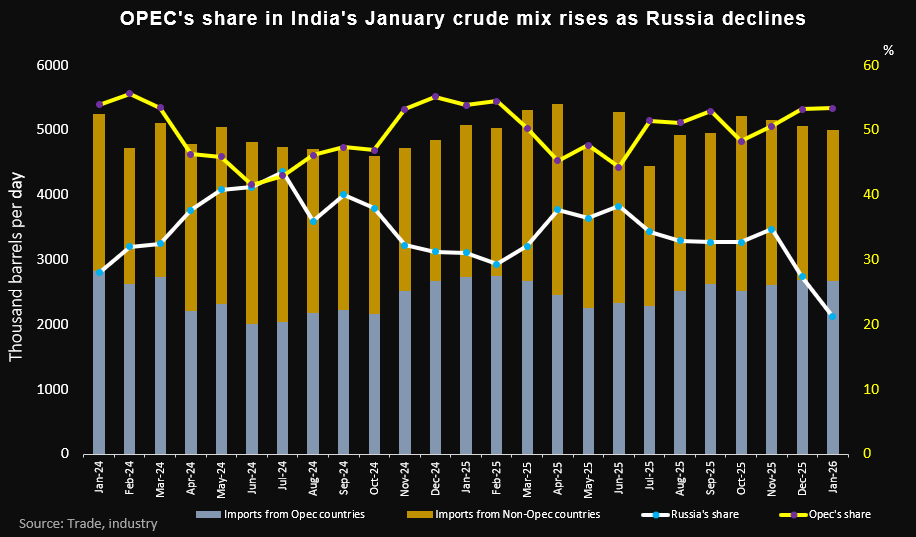

By mid-2023, Russia’s share in India’s crude imports jumped from barely 2% pre-war to nearly 35–40%. At peak, we were importing close to 2 million barrels per day from Moscow.

That wasn’t politics. That was math.

Cheap crude meant controlled inflation.

Cheap crude meant stronger refinery margins.

Cheap crude meant a manageable import bill in a $100+ Brent world.

But as of early 2026, that equation is shifting.

Russian imports have fallen sharply, while US crude shipments to India have surged nearly 80–90% year-on-year according to recent reports.

The question is simple:

Are we diversifying strategically, or absorbing higher structural costs?

The Russian Cushion: What We Actually Gained

India consumes over 5 million barrels per day and imports roughly 85–88% of its crude requirement. Oil is not just a commodity. It is a macro variable.

It influences:

- Inflation

- The Current Account Deficit

- The Rupee

- Industrial costs

Look at the trajectory:

- FY21 oil import bill: ~ $90 billion

- FY23 oil import bill: ~ $158 billion

- FY24 oil import bill: ~ $132 billion

Discounted Russian crude softened what could have been a much deeper macro shock.

The arbitrage was structured:

- Import discounted Urals crude

- Refine domestically

- Export diesel and aviation fuel at global prices

Indian refineries, optimized for medium-sour crude, expanded margins during this phase. Petroleum product exports surged. The system worked.

For three years, Russia functioned as a macro buffer.

Why the Pullback?

If the economics were favorable, what changed?

Three pressures:

- Sanctions compliance risk

- Payment settlement complexities

- Expanding US-India trade alignment

Energy trade does not operate in isolation. It sits inside diplomacy.

As trade negotiations with Washington deepened, sourcing patterns shifted. Russian volumes declined. US cargoes rose.

This is recalibration, not coincidence.

The Refinery Mismatch

Russian Urals is medium-sour crude. Heavier. Higher sulfur. Exactly what India’s complex refineries were designed to process.

US WTI Midland is predominantly light-sweet crude. Cleaner, but structurally different.

India’s demand profile remains diesel-heavy.

Excess light crude requires blending with heavier grades to maintain output balance.

Blending increases cost.

Margins compress.

The deep arbitrage of 2022–2024 does not translate seamlessly into a US-heavy basket.

The Dollar Factor

Russian trade experimented with alternative settlement routes, reducing direct dollar exposure.

US crude is dollar-settled.

If 1 million barrels per day shift from discounted Russian crude to US crude priced even $8 higher per barrel, that implies roughly $3 billion in additional annual outflows.

At scale, this affects:

- Current Account Deficit

- RBI intervention needs

- Rupee stability

Energy procurement quietly becomes currency management.

Freight and Landed Cost

Russian cargo routes were shorter and negotiated differently.

US Gulf Coast shipments involve:

- Longer transit times

- Standard insurance frameworks

- Higher freight costs

Small differences at scale compound significantly.

Inflation Transmission

Retail fuel prices in India are tax-managed, so crude price changes do not immediately reflect at the pump.

But structural cost increases eventually transmit into:

- Transport

- Fertilizer subsidies

- Manufacturing

- Core inflation

A sustained $5–10 per barrel increase can translate into 0.3–0.6 percentage points of inflation over time.

You may not see it instantly. You feel it systemically.

Strategic Diversification or Costly Realignment?

Between 2022 and 2024, India optimized for price advantage.

In 2026, it appears to be optimizing for geopolitical insulation.

The Russian phase protected margins and softened inflation during turbulence.

The emerging American phase strengthens diplomatic positioning but potentially narrows refinery margins, increases forex exposure, and reduces pricing leverage.

Energy economics is not just about barrels.

It is about leverage.

And the coming years will reveal whether this pivot strengthens India’s bargaining power or gradually dilutes it.

Sources

-

LiveMint: India’s Russian oil imports fall 18% in 2025; US crude shipments surge 83%

-

Carnegie Endowment: The Impact of US Sanctions and Tariffs on India’s Russian Oil Imports

-

Financial Express: Russian oil flows to India slump as EU curbs bite

-

Reuters: OPEC regains share as India’s Russian oil imports slump

Subscribe to Economic Frictions

Get independent analysis delivered to your inbox.

Instant unsubscribe link included in every email.

Secure Subscription • One-Click Unsubscribe