What if survival is what we call growth?

There are a few friends of mine who use their credit cards to maintain their current lifestyle. It’s normal for them to use it for clothes, food, and even other expenses. Till that point, it’s fine.

But the problem occurs when they use another credit card and pull money from it to pay for the first credit card so as to not default. In this process, what they generally forget is that they do not get the exact amount they pulled. Moreover, when converting to an EMI (Equated Monthly Instalment), the bank asks for some conversion charge along with GST, and on top of that, they also ask for the interest. So anyhow the individual involved in this might get what they want, but their debt keeps on increasing.

Let’s go towards it mathematically

Assume I have a credit card and I have a certain limit, but I bought goods and services costing ₹10,000. Now, in order to not default, I take another credit card and pull an amount of ₹10,000 from that bank’s card.

As per the regulations, the merchant payment fees lie between 1-3%, so it costs between ₹100-₹300 for this transaction. If we take into consideration the option of EMI which is 14-22% per annum interest rate and charges ranging from 1-3.5%, that makes up for ₹774-₹1,231 in costs, plus GST from ₹139-₹222.

At an individual level, the amount may not appear large. But aggregated across many households over a financial year, it becomes substantial. When repeated month after month by the same individual, what initially feels like liquidity gradually turns into a persistent burden.

Let’s talk economically

At the individual level, credit typically serves two purposes: to manage urgent needs or to smooth consumption over time. When used within these limits, borrowing can stabilise households and support economic activity. Problems arise when credit begins to substitute for income on a persistent basis, quietly transferring today’s consumption burden into the future.

This dynamic is particularly relevant in a country like India, where income distribution is highly uneven and financial buffers vary sharply across households.

- For lower-income groups, borrowing is often driven by necessity and sourced from informal or semi-formal channels, where effective interest rates are high.

- For middle-income households, credit increasingly supports the maintenance of living standards rather than their expansion.

- At the top end, credit is more often used strategically for leverage, investment, or liquidity management.

As a result, the same instrument credit has very different economic effects across income groups. Inflation raises the cost of essential consumption, per capita income growth remains uneven, and GDP growth aggregates spending without distinguishing its source. Consumption may remain strong in the data, even as household savings thin and future income becomes increasingly committed.

The risk, therefore, is not immediate collapse but rising fragility. How? As inflation keeps rising and from my previous work, income has a lag effect rather than inflation this leads to reduced real income. This means one must obtain resources either by working more or through credit.

When credit is available to every household through small finance banks, credit cards, or similar channels, households often choose this route for survival or maintaining their livelihood without considering the foregone future income. In a country like ours where income is so unequal, so is the need for credit. When credit might be a necessity for one, it might be an opportunity for another.

Let’s back it up statistically

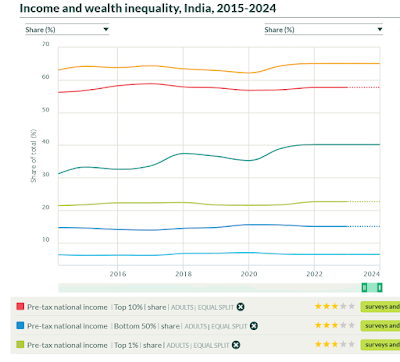

1. Income Inequality

Income distribution remains sharply uneven, meaning the ability to absorb shocks is not uniform.

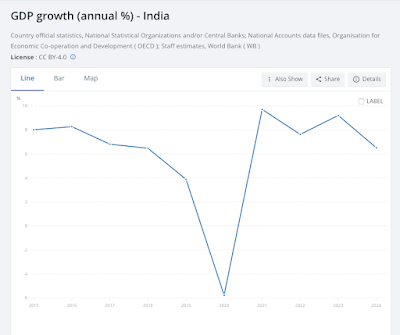

2. GDP Growth (Annual %)

The economy is expanding in aggregate terms.

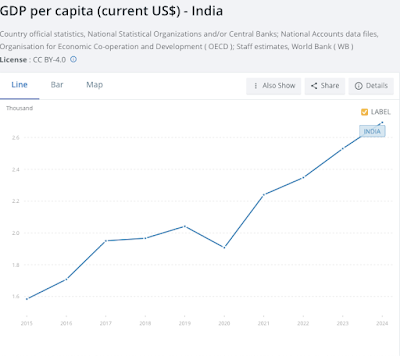

3. GDP Per Capita

Broad upward trend over the long run.

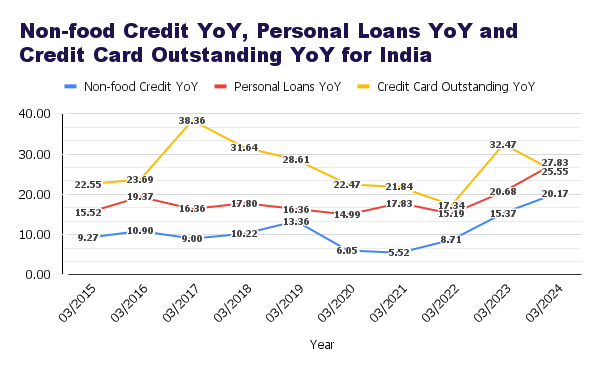

4. Credit Growth vs Personal Loans

The strong rise in personal loans and credit card outstanding growth signals spending funded by debt.

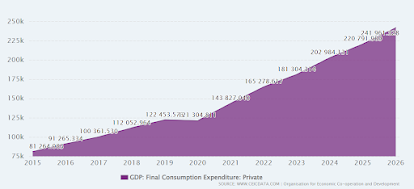

5. Private Final Consumption Expenditure

Consumption remains strong, but likely funded by borrowing capacity.

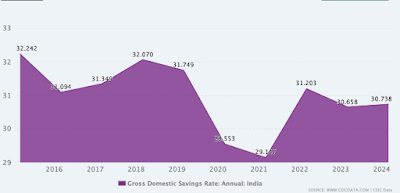

6. Gross Domestic Savings Rate

Savings are falling or remaining weak while credit expands.

Final Interpretation

Taken together, these graphs show that India’s macroeconomic story can look stable and even improving on the surface, while household-level financial pressure quietly builds underneath.

The inequality chart highlights that income distribution remains sharply uneven across the period, meaning that the ability to absorb inflation or shocks is not uniform most households do not experience “growth” in the same way aggregate numbers suggest. At the same time, the GDP and per-capita income graphs indicate a broad upward trend over the long run, which supports the idea that the economy is expanding in aggregate terms.

However, the crucial shift appears when we observe the credit-side indicators: the strong rise in personal loans and especially credit card outstanding growth often outpacing broader non-food credit growth signals that a growing portion of household spending is being supported by short-term and unsecured borrowing rather than purely by income expansion.

This becomes even more meaningful when seen alongside the consumption expenditure chart, which rises steadily: consumption remains strong, but the credit graph suggests that part of this strength may be funded through borrowing capacity, not improved financial security. The savings rate chart strengthens this conclusion further when savings fall or remain weak while credit expands, it implies that households are maintaining expenditure with thinner buffers, making them more sensitive to future shocks.

In this structure, “growth” can continue to appear healthy in GDP and consumption data because those indicators capture spending, not the financial strain behind it; yet at the household level, repeated borrowing converts present stability into future repayment commitments. Therefore, the combined message of these graphs is not that India is collapsing, but that resilience is increasingly being financed where a section of households may be borrowing not to upgrade their standard of living, but simply to maintain it.

When consumption is sustained by rising unsecured credit amid persistent inequality and weak savings, what looks like growth in aggregate can, for many households, be better described as survival with a delayed cost.

Sources: RBI Data, WDI, CEICDATA

Subscribe to Economic Frictions

Get independent analysis delivered to your inbox.

Instant unsubscribe link included in every email.

Secure Subscription • One-Click Unsubscribe